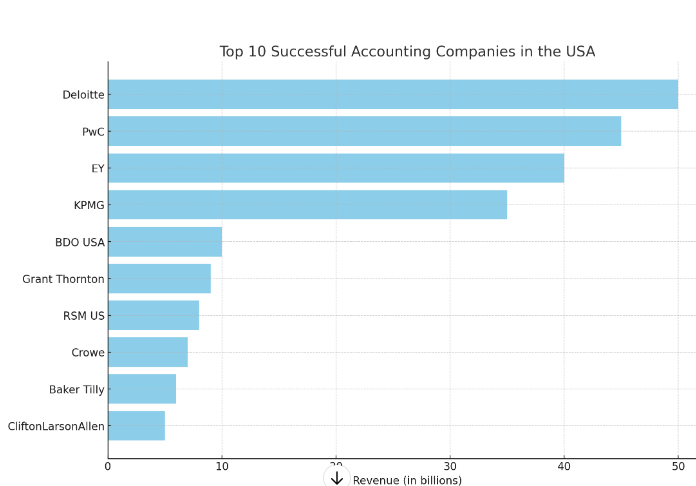

The Three Basic Accounting Principles

Principles for Successful Companies

- Introduction

- The Foundation of Accounting Principles

- The Revenue Recognition Principle

- The Matching Principle

- The Historical Cost Principle

- The Value of Practical Applications and Importance

- Practical Application of the Revenue Recognition Principle

- Practical Application of the Matching Principle

- Practical Application of the Historical Cost Principle

- Additional Vital Accounting Rules

- Conclusion

- Other Essential Accounting Principles

The Three Basic Accounting Principles for Successful Companies

Introduction

Any thriving business owes its success to accounting, which supplies the vital framework for managing a company’s finances and making high-level decisions. Because it’s so important that a company’s financial data be accurate and meaningful, accountants rely on a core set of rules to govern how we work. In particular, there are three key rules that we can think of as underlying the entire double-entry accounting system.

The Foundation of Accounting Principles

The foundation of accounting is grounded on three inalterable basic principles. These rules are known by any good accountant and should well be understood by any business major. In this report, we will meditatively heed to core accounting rules, in terms of three components that produce a sum; there’s a sum that has to be reached through certain conditions, and the sum, once reached, has to be both stable over a certain period and not easily alterable. This series of sufficient conditions doesn’t make for exciting work, but it’s supposed to be accurate, in a thousand-dollar-error sort of way, if a few cents aren’t at stake.

The Revenue Recognition Principle

The Revenue Recognition Principle holds the right to rule when recording revenue in financial statements. Nonetheless, it is really straightforward: recognize revenue when you earn it!—with one important wrinkle. From a business’s financial standpoint, “earn” means an almost equivalent word: “obligate.” A business incurs an obligation when it delivers to me the MacBook Pro it promised. If it fails to make good on this implicit promise, I can take it to court and be almost certain of winning—unless, like The Beatles, a business’s failure was caused by an “Act of God.” When the business delivers the promised goods to me or performs the promised service, then it essentially has incipient rights to a claim against me for the money it expects to receive. It’s not just straight-line “earning.” Obligation is a crucial component.

The Matching Principle

The Matching Principle: The Matching Principle is in lockstep with the Revenue Recognition Principle, performing a kind of pas de deux. It functions mainly to ensure that expenses are recognized, or “counted,” in the same period as the revenues that the expenses have supposedly helped to generate. Expenses can sometimes, however, be hard to recognize. By comparison, revenues are recognized when the outcomes of certain ventures to which a firm has committed are realized in forms that can be counted. And because the recognition of revenue is, at the same time, the premier occasion in financial statements for realizing (recognizing) gains of the kind that a business is supposed to achieve.

The Historical Cost Principle

The Historical Cost Principle requires that, with some exceptions, an entity record transaction prices at the point of first asset acquisition. This entry point is recorded as the historical cost and serves as the basis not only for initial valuation but also for any subsequent valuation. In effect, the Historical Cost Principle commands an entity to use the transaction price when making its financial representations—despite the fact that price is different when the asset is first acquired from the prices that can be acquired (or paid) in subsequent transactions. Once the asset is first put “on the books,” the entity keeps the assigned display there until some consummation measure is reached (Hendriksen and Van Breda 2007; Walton 2000).

The Value of Practical Applications and Importance

In my opinion and experience, education is of absolutely no use if you cannot apply it practically. What is the point of having knowledge if you cannot utilize it to solve real-world problems? I have seen firsthand the difference between students who went far in their science and mathematics skills versus those who could simply learn the necessary information needed to do well on a test but faltered when it came to finding solutions in an actual context.

Practical Application of the Revenue Recognition Principle

Let’s dive into where we can actually use these and why each of these fundamental accounting rules is important, okay?

The Revenue Recognition Principle in Action

Picture a software company that you pay an annual subscription for. The company ought to recognize your subscription as revenue in its statements of profit and loss. But over what period should it perceive that subscription as revenue? If the software company offered quite literally nothing to the subscriber other than the fact of the subscription, it might recognize the revenue over the period of the arrangement (that is, over the side of the period that doesn’t quite happen to the appearance of the paper).

Now, what should happen if the onus is actually on the software company (and not the subscriber) to offer service during this annual period? Apparently, the company might be bound to do so in return for the revenue that it recognizes monthly from the here-and-now of the subscriber’s very appearance, at least for some notional portion of what the service doesn’t actually provide.

Practical Application of the Matching Principle

The matching principle allows a company to record the expenses necessary to produce goods in the same period of time as the associated revenue from selling the goods. For a company that manufactures products to order, like a custom guitar shop, this means recognizing all the costs and all the revenues in the same accounting period. The cost of making the electric guitar is “matched” with the sale of the custom electric guitar. The only time a cost isn’t recognized is when the finished good isn’t sold, in which case the cost becomes part of the “ending inventory” on the balance sheet.

Practical Application of the Historical Cost Principle

The Historical Cost Principle comes into play when, for instance, a real estate investment company buys a commercial property for $1 million. That property is initially written up on the company’s balance sheet as an asset worth $1 million. Its value may rise or fall after the acquisition due to changes in the market or the appearance of new advantages or disadvantages in the local economy, but as long as the building’s value doesn’t need to be “impaired,” as accountants like to say, it stays on the papers at the same $1 million. And, as a rule, you’d think that if a building’s value went up, the company would be smart to write that up, too, wouldn’t you? But that’s not the way accountants-online-dating works. They have a date with the valuation of assets at the asset’s acquisition cost, and the date usually stops there. For the benefit of providing a more reliable foundation to the company’s stakeholders, the appearance of management’s choice to use the HCP does give a choice to use the reliable figures they are recording unless the appearance of what is now known as asset impairment comes into play.

Additional Vital Accounting Rules

There are other vital accounting rules besides GAAP. To function properly, any accounting “language” also needs a set of agreed-upon definitions for common terms and documents. For example, financial statements must have a standard format that can be followed to compare one firm’s financial status with another’s. Similarly, when the word “asset” is used, everyone must be very clear about what is and what is not an asset. Imprecision or loose interpretations can wreak havoc. Accounting is like a game of “Monopoly” — you have to know the rules to play. But unlike the board game, in the real world of accounting, not knowing the rules, or choosing to ignore them, can have very serious consequences.

Conclusion

The bedrock of reliable accounting practices consists of several foundational principles, with the main ones being the Revenue Recognition Principle, the Matching Principle, and the Historical Cost Principle. To form the upper structure of the rock-solid base of accounting, you should start with these three. Once you’ve mastered these (and hopefully, you will never have any occasion to commit them to memory), you can move on to other rules and guidelines that work over and above the basic principles.

Other Essential Accounting Principles

The Principle of Conservatism

The principle of conservatism instructs accountants to lean towards caution in all matters of doubt within the world of financial reporting. The point is not that they should think of the worst-case scenario but that they should resolve any ambiguity in a way that errs on the side of understatement rather than overstatement. In doing this, the company makes sure that it isn’t building up a “cookie jar” of overstated earnings to reach into during tough times. Instead, it’s spreading out the bad news over a longer period.

The Consistency Principle

The consistency principle makes sure that when you look at a company’s financial statements one year and its financial statements for the next year (except where changes in practices, principles, or estimates have been declared in footnotes), you can do a meaningful year-over-year comparison. A company performed a certain way this year. Did it do better or worse than last year? The CEO made a statement that the company performed in a certain way. Did it really happen? This can only be confirmed after the financial statements have been audited, buffed, and shined. Another way of saying “this really happened” is to say “these figures are reliable.”

The Materiality Principle

The Materiality Principle holds that financial information should be presented if, and only if, it is sufficiently important that its presence, its very absence, even distortion, or its lack of visibility, could influence the decisions to be made in using that information. So we have a standard that governs the provision of financial information, one meant to ensure the satisfaction of a number of conditions and the avoidance of certain negative consequences.

The Full Disclosure Principle

The Full Disclosure Principle mandates that clear, open, and honest financial records and statements be kept, in order to provide all stakeholders (e.g., stockholders and potential stockholders, especially) with the information they need to make decisions. This principle is concerned with including everything that might be necessary for understanding what has been happening and makes it clear that there should be no ‘disguising’ of what has been going on.

Leave a Reply